CHIP Funding Cuts Would Leave 8M Low-Income Kids Uninsured

Failing to extend CHIP funding would raise care costs and leave millions of low-income children without insurance coverage.

Source: Thinkstock

- More than 8 million low income children living with chronic diseases would lose healthcare coverage and incur higher costs if CHIP funding is not extended beyond 2017, says new research from the Yale School of Medicine.

In a study published in Health Affairs this month, researchers found that the families of these children would face annual out-of-pocket costs ranging from $233 at the lowest income levels of 100-150 percent of the federal poverty level (FLP), to $2,472 at the highest income levels if they are forced to move from CHIP plans to coverage available through the health insurance exchanges.

CHIP is critical for providing care to millions of low-income children otherwise ineligible for Medicaid, and is currently protected by federal policy through 2017.

However, “more than eight million children could have their health insurance disrupted if federal funding for CHIP is not extended,” the research team warned.

“In this study we explored policy alternatives of extending federal funding for CHIP or enrolling children in the existing health insurance Marketplace. As currently configured, both CHIP and Marketplace plans offer generous protections against high out-of-pocket expenses compared to being uninsured. When comparing CHIP and Marketplace plans, at all income levels, CHIP provides better protections against high out-of-pocket spending for families of children with chronic conditions.”

The team analyzed claims for 7,266 children with at least one chronic condition. The sample found that children with a chronic condition spent an average of $3,361 in annual healthcare services.

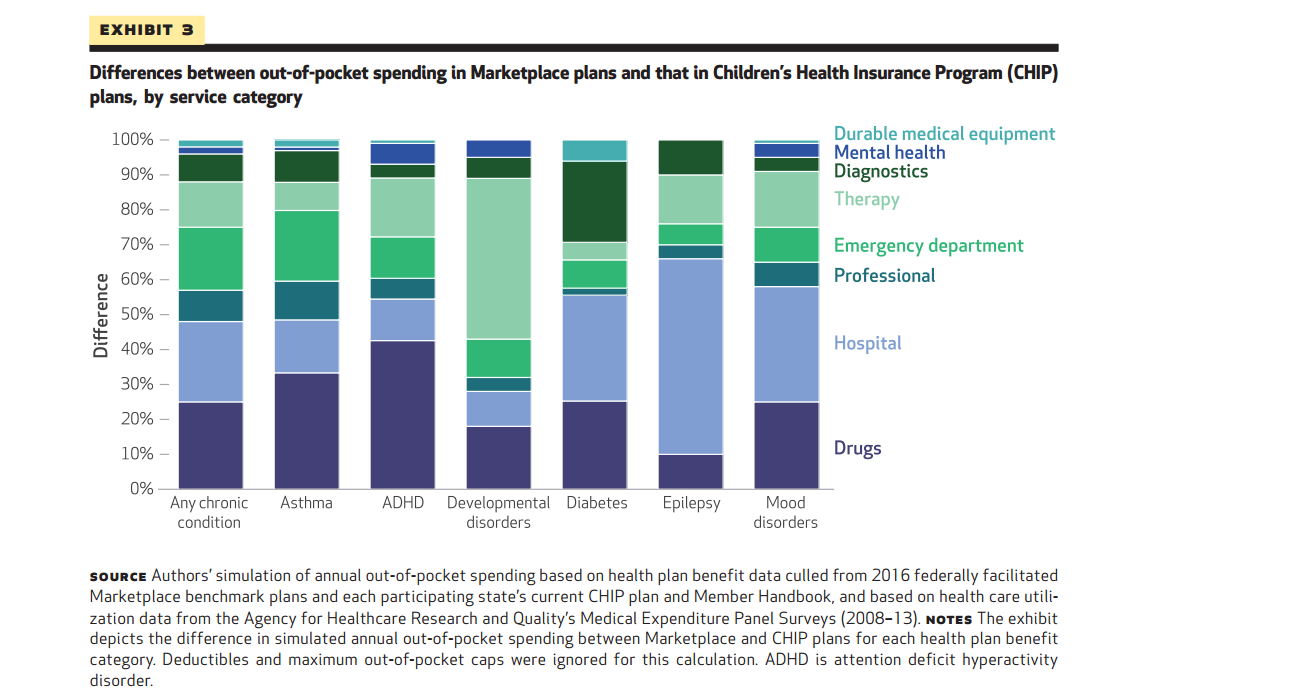

For these children, the largest expenditure categories per child included prescription drugs (29 percent), inpatient hospitalization (20 percent), and professional services (20 percent). The final results of the analysis compared CHIP expenditures to Marketplace plans.

Through health plans offered by CHIP, families at 100-150 percent of the FLP who qualified for assistance avoided Marketplace deductibles of $178. Marketplace deductibles rose as high as $3,126 for higher income families.

Out-of-pocket spending for average CHIP enrollees totaled at $26 for families between 100-150 percent below the FLP, which was $233 dollar less than Marketplace out-of-pocket costs. At higher level incomes, the CHIP families averaged out-of-pocket costs of $74 dollars compared to $1,552 for Marketplace plans.

When the researchers broke down out-of-pocket spending by care categories, children’s out-of-pocket costs for drugs under Marketplace plans were 25 percent higher than CHIP for treating any chronic condition.

Source: Health Affairs

Three possible policy-based solutions the research team proposed could make Marketplace plans comparable to CHIP plans.

The first of the proposed solutions includes enhancing cost-sharing protections at income levels around 200-250 percent of the FLP. The research team believes this will help close the gaps between out-of-pocket costs based on income level.

Another solution involves adjusting policy to help limit the cost sharing growth rate of prescription drugs and hospitalizations, the two highest spending categories for children with chronic conditions.

Finally, the researchers suggest that monitoring the cost of deductibles can help identify adverse effects on affordability, quality of care, and access of care.

Even with these policy strategies in place, however, the researchers believe that reauthorizing funding is the most effective method to make sure these low-income children receive affordable care.

“These strategies presume a robust health insurance Marketplace and small modifications to the ACA,” the team concluded. “Given concerns about the viability of the Marketplace, the legal battles regarding the cost-sharing reduction payments, and the efforts to repeal the ACA, reauthorizing funding for CHIP is most likely the least disruptive strategy moving forward.”