Court Sides with Republicans on Affordable Care Act Provision

The future of the Affordable Care Act depends upon the appeals process and whether the Obama administration does or does not have the authority to grant cost-sharing reductions.

- Once again, the Patient Protection and Affordable Care Act is receiving criticism from the Republican-led House of Representatives. House Republicans had filed a lawsuit claiming that the Obama administration does not have the authority to provide cost-sharing reductions for low-income individuals who purchase health plans on the insurance exchange.

The American Hospital Association (AHA) reported last week that a federal district court judge agreed with the House Republicans and ruled against the government’s authority to reimburse cost-sharing reductions in House v. Burwell. These tax subsidies are essential for ensuring that the individual mandate and goal of greater healthcare coverage continues. The subsidy program does have the opportunity to continue appealing the Court's ruling.

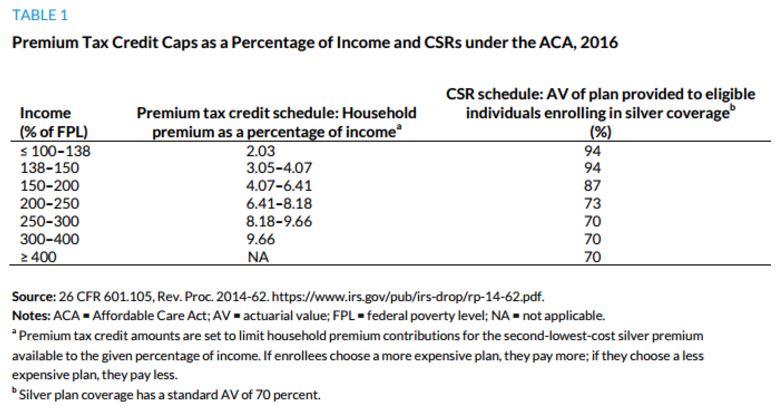

House Republicans stated in the filed lawsuit that Congress did not give authority to a line-item appropriation of these cost-sharing payments. These cost-sharing reductions are given to families and individuals who have incomes between 100 percent and 250 percent of the federal poverty level. These consumers must also be enrolled in silver health plans.

“The AHA is disappointed with the court’s decision denying cost sharing assistance to low-income individuals who buy their health insurance on the federal health exchanges,” Melinda Hatton, Senior Vice President and General Counsel of the American Hospital Association, said in a public statement. “Today’s decision could be a setback for those who need affordable healthcare insurance, because we are concerned that it could lead to increased premiums. We will file an amicus brief as part of the appeals process.”

Prior research from the Urban Institute shows that, if the ruling stands, the cost of premiums for silver plans will increase by more than $1,000. If the cost-sharing reductions are abolished on the health insurance exchange, this would be a huge blow for the Affordable Care Act since it would limit the amount of families who have health insurance and greater access to medical care.

In its report, the Urban Institute used its Health Insurance Policy Simulation Model to analyze the exact implications of a ruling that would put an end to federal reimbursement of cost-sharing reductions. First, it is important to note that health insurance companies would adopt higher premiums in their silver plans in order to offset the costs associated with cost-sharing reductions.

The Affordable Care Act and the health insurance exchange could become obsolete for consumers who purchase silver plans since these policies would essentially become unaffordable and out of reach if the federal district court's ruling stands. The urban Institute found that silver plan premiums would increase an average of $1,040 per person.

Additionally, if the premiums increased drastically, the federal government would have to pay higher amounts for Marketplace tax subsidies. This type of reimbursement is linked to the second-lowest-cost silver plan premium. Essentially, this would lead to an unsustainable system and would severely restrict the Affordable Care Act.

Consumers who are eligible for these tax subsidies and have incomes up to 400 percent of the federal poverty level would end up receiving higher payments from the tax credits because of the increase in premium price. This federal district court ruling would negatively impact the government’s budget and may increase taxes around the country.

The health insurance exchange would end up losing approximately 1 million enrollees because of these consumers would not Be eligible for tax subsidies and could find affordable healthcare coverage elsewhere.

This court ruling could also greatly impact the decision of payers to continue selling policies on the health insurance exchange. Since UnitedHealthcare has decided to leave state-based health insurance marketplaces in 2017, it is possible that more payers could end up dropping out of the exchange especially if the court ruling stands.

“An ultimate finding for the plaintiff in House v. Burwell would prohibit federal reimbursement of insurers for the CSRs they are required by law to provide to low-income Marketplace enrollees unless Congress specifically appropriates the funds to do so,” the report from the Urban Institute commented.

“In such a case, were there to be no explicit appropriation, a finding in favor of the House of Representatives could cause significant disruption to the ACA’s nongroup insurance Marketplaces, depending upon the timing and notice provided to insurers.”

“Without sufficient notice, insurers would be unable to change their approved premiums, causing them to choose among incurring significant near-term financial losses, abruptly leaving the Marketplaces, filing their own legal actions against the federal government, potentially violating notice requirements for exiting the Marketplaces, and causing enormous disruption to their enrollees.”

If these drastic changes to the latest healthcare reforms were to occur, there will need to be a system in place to substitute medical coverage and ensure greater healthcare access among low-income families. The future of the Affordable Care Act depends upon the appeals process and whether the Obama administration does or does not have the authority to grant cost-sharing reductions.

Image Credits: Urban Institute

Dig Deeper: