Health Insurance Exchange Consumers Satisfied with Health Plans

Individuals who purchase plans on the health insurance exchange tend to use online resources to shop for a policy at twice the rate as the average consumer.

- Despite the fact that the House of Representatives and the Senate attempted to repeal the Affordable Care Act at the end of 2015, consumers seem to be satisfied with their healthcare coverage options after purchasing health plans on the health insurance exchange, according to a new study from Deloitte Consulting LLP.

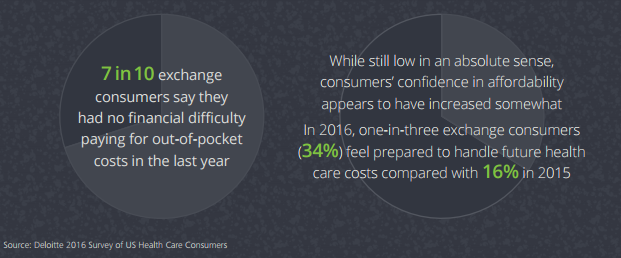

Additionally, the report found that more consumers are ready to take on future medical costs and are more confident about accessing affordable healthcare services than in 2015. It was also uncovered that consumers who purchase plans on the health insurance exchange tend to use online resources to shop for a policy at twice the rate as the average consumer who obtains employer coverage.

In fact, the Deloitte report discovered that most consumers using the health insurance exchange were not surprised by their out-of-pocket costs, which shows that these individuals have done the research and gained the knowledge necessary to purchase the best health plans for their needs.

These consumers are also comparing and contrasting health plans as well as analyzing their total costs before purchasing a policy. Additionally, these individuals “continue to be willing to accept network tradeoffs for lower payments,” the report stated.

As reported in a Deloitte press release, those who purchase coverage on the health insurance exchange exhibit characteristics of smart shoppers. These consumers are also just as happy with their health plans as those who obtain employer coverage.

“We’re witnessing the continuing evolution of a more consumer-centric model of healthcare, and the ways in which consumers are navigating the exchanges provide evidence of that,” Greg Scott, Principal of Deloitte Consulting LLP, said in a public statement. “Health care consumers’ expectations for information and transparency are increasing, as is their interest in intuitive tools to access relevant information. Meeting these expectations should lead to increasingly more confident and satisfied customers in the future.”

However, the report did uncover that Medicaid and Medicare beneficiaries are more satisfied with their healthcare coverage than those purchasing plans on the health insurance exchange.

Seven out of ten exchange consumers polled in the study stated that they managed their out-of-pocket costs over the last 12 months without major issues cropping up. Only 25 percent stated that their out-of-pocket costs were higher than they anticipated. Nonetheless, consumers and families operating on lower incomes said that they found it challenging to pay for their out-of-pocket costs.

“Out-of-pocket costs have been increasingly top-of-mind for healthcare consumers as the nature of insurance has changed over the past several years,” Paul Lambdin, Director of Deloitte Consulting LLP, stated in the press release. “This cost issue appears to be making exchange consumers pay close attention to the details of their coverage, and changes in benefits and premiums year over year.”

Even though it seems that consumers have benefited from the health insurance exchange and the Affordable Care Act, the health insurance industry as a whole may be suffering from these new regulations. UnitedHealthcare, for instance, has reported major financial losses and will be leaving state-based health insurance exchanges in 2017.

One report from the Mercatus Center at George Mason University states that payers have been hit with significant financial losses on a per-enrollee basis due to the provisions of the Affordable Care Act. Even though health insurance companies received net reinsurance payments of $6.7 billion or $833 per enrollee, payers suffered from a net loss of more than $2.2 billion in 2014, the report finds.

Since there were fewer enrollees in the health insurance exchange than expected two years ago, the reinsurance program was established to provide 40 percent more funds than originally planned. Despite this, there was a total net loss among insurers of more than $2.2 billion for individual market quality health plans in 2014.

“Insurers incurred large losses in 2014 despite receiving $6.72 billion in net reinsurance payments for their individual market QHPs [Qualified Health Plans]. The average loss ratio (medical claims paid divided by premium income) for the 289 QHPs equaled 1.110 when weighting QHPs by claims. This loss ratio suggests that premiums for individual market QHPs will have to rise significantly when the reinsurance program ends. Assuming that insurers generally need at least 15 percent of premiums to cover administrative expenses, premiums in 2014 were roughly 26 percent too low, on average, to cover insurers’ full costs of offering individual market QHPs,” the report stated.

“If average premiums had been 26 percent higher, however, that would have lowered total enrollment and increased selection effects. Relatively healthy people and higher income enrollees, who qualify for little or no subsidies that make the insurance more attractive, would have been deterred to a greater degree than people who expected to use more healthcare services. As a result of this dynamic effect, the average premium increase would likely have needed to be substantially greater than 26 percent for insurers to break even on their QHPs in 2014.”

The report also found that payers with narrow networks were more successful when operating through the health insurance exchange. The risk pool currently hitting the market is very different than before due to the ACA’s stance on mandating universal coverage. At this point in time, financial data from 2015 appears to be similar to the findings from 2014.

This is problematic, as it indicates payers may not be able to function sufficiently within the exchanges. There may need to be regulatory changes to ensure payers remain profitable and capable of offering coverage to these populations.

Dig Deeper:

Risk Adjustment Affects Plans on Health Insurance Exchanges

Consumer Engagement Vital in Health Insurance Exchanges