How the Medicare Advantage Market Can Offer Payer Opportunities

The Medicare Advantage market is ripe with payer opportunities in the form of profitability, open competition, and a strong consumer base.

Source: Thinkstock

- Medicare Advantage (MA) market data from A.M Best and the Kaiser Family Foundation reveals that the MA market has remained profitable and provides financial opportunity, but payers looking to enter into the market should expect to address developing challenges in revenues, financial solvency, consumer satisfaction, and competition

MA double-digit premium growth rates have been regular the last ten years, reaching as high as 22 percent in 2011 and 20 percent in 2014. Expected MA premium revenues have tripled since 2007 as they grew from $69.9 billion to $187.5 billion in 2016.

Payers have a consistently growing market option through MA products, as the segment’s total net premiums earned grew by 7 percent, from 16.6 percent in 2007 to 23.9 percent in 2016.

While the profitability of MA plans may be enticing for payers eager to enter the market, there are some challenges in regards to competition and market saturation.

At a national level, the market is heavily concentrated, as the top three players UnitedHealth Group, Humana, and the Kaiser Foundation Group of Health Plans account for 50 percent of MA enrollment.

READ MORE: How Medicare, Medicaid, and CHIP Guide the Health Payer Industry

“Enrollment remains highly concentrated among a handful of firms both nationally as well as locally. For example, in 17 states, one company accounts for more than half of all MA advantage enrollment, indicating that some markets are much less competitive than others. In addition, 47 states have more than half their MA enrollment placed with just two companies, and 31 states have two-thirds of their enrollment in two companies.”

The largest leaders of the 2016 MA market included UnitedHealth (20.5 percent), Humana (19.5 percent), Kaiser Foundation (10.3 percent), Aetna, Anthem, Cigna, Highmark, Centene, Wellcare, and BCBS of Michigan.

However, there are plenty of opportunities for smaller payers to get into the mix, as the potential MA consumer base has steadily grown over the years.

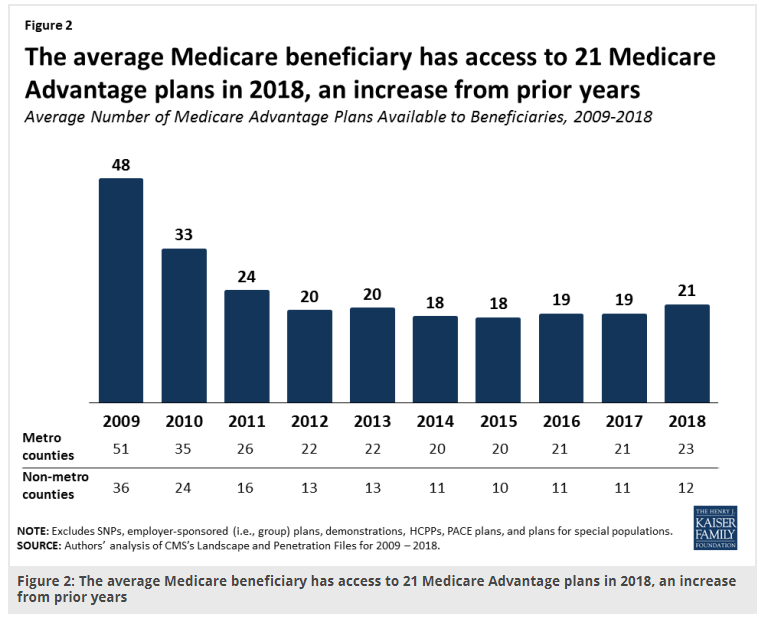

The number of available MA plan options in the US grew from 2,034 in 2016 to 2,317 in 2017, and the average MA beneficiary will have access to 21 different MA options. Eighteen of those plans also include prescription drug coverage plans, or MA-PDs, which was a slight increase over the previous year.

Source: Kaiser Family Foundation

Historically, MA plan access has remained stable for consumers as 99 percent of Medicare beneficiaries will have access to either a MA HMO, PPO, PFFS plan, or a regional PPO.

READ MORE: Medicare Advantage Premiums Drop 13% Due to Affordable Care Act

In 2018, however, Medicare Advantage plans will unavailable in 149 counties during 2018 in parts of the mid-west and northwestern regions of the US, offering new entrants an opportunity to fill these gaps.

The average Medicare beneficiary in 2018 will be able to choose a MA plan from six payers. Seventeen percent of Medicare beneficiaries nationwide will be able to choose plans from 10 different payers, and another 21 percent of beneficiaries only have three or less payers to choose from.

Payers that are able to expand their offerings and enter into MA markets may have to take extra time to develop health plans with high consumer satisfaction rates, which can be highly marketable and additional profitability through CMS’s star rating system.

Recently, many payers have begun to offer $0 premium MA plans alongside other benefit plans with moderate to high premiums, leveraging both premium revenues and CMS bonus payments received for plans with four or more stars.

The number of MA contracts rated four stars or higher has increased gradually, from 38 percent in 2014 to a high of 49 percent in 2016, before declining to 44 percent for the 2018 plan year. In 2016, margins improved materially, with 42.8 percent of companies reporting positive margins giving some credit to their high Star ratings.

READ MORE: What Are the Pros and Cons of Consumer Driven Health Plans?

“In many regions, carriers offer $0 premium MA products, which are very attractive in the market to seniors, so insurers will work hard to minimize the need to charge members premiums above the payments they receive from CMS,” the A.M Best report added. “A carrier’s size can be a determinant of certain factors affecting costs and benefits, such as administrative expenses and provider reimbursement.”

Because there has been a moderate decline in star ratings, the payers that develop higher quality MA plans may be able to offer a considerably more marketable product. Fifty two percent of MA enrollees chose plans with four or more stars in 2014, and that number increased to 73 percent of enrollees in 2018.

The MA market remains an opportunity, but will require new cost-management and revenue solutions as it becomes more crowded and competitive with eager market entrants.

“The MA market will continue to evolve, with the pressure on revenue increasing owing to the ACA, the competitive market, and other regulatory changes,” A.M Best concluded in their report.

“Insurers will likely see more cost and revenue challenges in the coming years, and additional expenses could shift to the members through benefit reductions or premium increases, or plans could stop offering products in certain markets if they are unable to achieve profitability.”