Payer Concentration Challenges Health Insurance Exchanges

Studies are showing that greater concentration of health plan issuers is posing a problem for state health insurance exchanges.

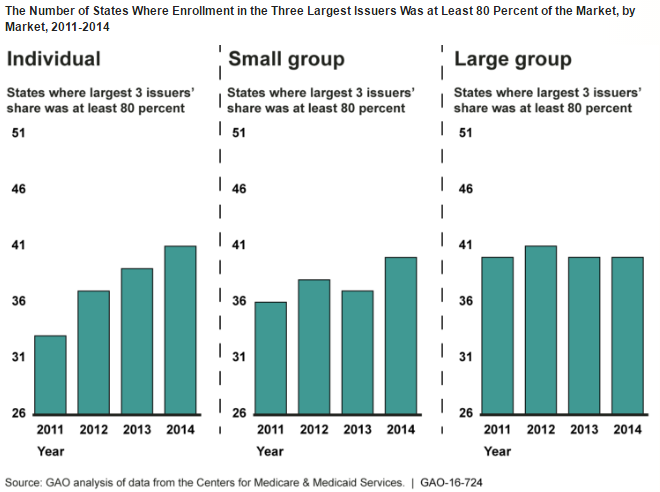

- More and more research is pointing at the fact that consumers on the health insurance exchanges are being left with fewer health plan issuers. Part of this may be due to health payers such as UnitedHealthcare or Aetna leaving a large percentage of the market. However, even in previous years, the largest national payers held more of the health insurance market. A report from the US Government Accountability Office (GAO) found that the three largest issuers held 80 percent of the market in most states from 2011 to 2014.

Starting in 2014, however, the Affordable Care Act gave health plan issuers the opportunity to sell health plans to individuals ineligible for employer-sponsored coverage through the health insurance exchanges. The report outlines that some of the exchanges had less than three issuers participating.

The GAO researchers looked at three types of markets that health plan issuers participated in, which include individual, small group, and large group. The results show that the number of payers who participated in individual markets dropped from 2013 to 2014. Small group and large group participation remained relatively steady during this same time period within most state health insurance exchanges.

“We analyzed 2011 through 2014 Medical Loss Ratio (MLR) data that PPACA [Patient Protection and Affordable CAre Act] requires issuers to report annually to CMS. We used the same data source that we used in the previous report, and we updated our analysis with 2014 data, which were the most recently available at the time of our review. Specifically, we identified enrollment data for the issuers that offered coverage in each state’s overall individual, small group, and large group markets,” the report stated.

“Although multiple health issuers participated in each state’s individual, small group, and large group health insurance markets from 2011 through 2014, the markets remained concentrated during this time period. On average in each state, there were between 22 and 30 issuers participating in the individual market each year during the time period and there were between 11 and 14 issuers participating in the small group and large group markets. However, market share was generally concentrated among few issuers in each of the 4 years we examined and became more concentrated in the individual and small group markets over the time period.”

Issuers that had left the market before 2014 usually had less than 1 percent of each state market, according to the GAO report. Additionally, there were new health payers that entered the playing field in 2014.

Prior research from GAO indicated that there was a very concentrated health insurance market from 2010 to 2013, which may point to less competition among payers and the potential for fewer benefits and higher premium costs among consumers.

However, the Affordable Care Act brought forth health insurance exchanges and other types of healthcare reforms that were meant to transform payer concentration and stimulate competition between health plan issuers. While it would have been greatly beneficial if the Affordable Care Act actually incentivized the increase of competition within the health insurance market, the opposite may actually be taking place.

The stability of the health insurance exchanges may be falling behind since more studies have found that fewer payers will be participating on the exchanges in 2017 than in prior years.

For instance, the Henry J. Kaiser Family Foundation predicted in a new analysis that only 62 percent of enrollees will have the option to choose between three or more health plan issuers next year, which is a 23 percent decline from 2016.

Another important statistic found from the Kaiser report includes the fact that as many as 19 percent of marketplace consumers may have only one issuer available to them in 2017. While this report places the statistic at 19 percent, an analysis conducted by the McKinsey Center holds that number below at 17 percent of enrollees facing only one issuer in their relevant region.

Additionally, as many as five states will have only one health plan issuer operating within their individual health insurance exchanges. This type of monopoly could negatively impact consumers through higher out-of-pocket costs, increased monthly premiums, and fewer benefits.

Along with these studies, a policy brief from the University of Minnesota Rural Health Research Center found that, out of 2,512 counties analyzed, 7 percent or 175 counties had only one health plan issuer operating through the exchanges in 2015.

The federal government and the health insurance industry may need to work together to form more reforms and modifications to the Affordable Care Act in order to keep competition more robust in the market and, thereby, align more closely with consumer interests.

Dig Deeper:

How Payers Could Succeed in ACA Health Insurance Exchanges

7% of Counties Retain One Payer on Health Insurance Exchanges