Payers Face 9.6% Underwriting Loss on Health Insurance Exchange

Payers selling plans to individuals on the health insurance exchange experienced higher underwriting financial losses in 2015 than 2014, Milliman found.

Source: Thinkstock

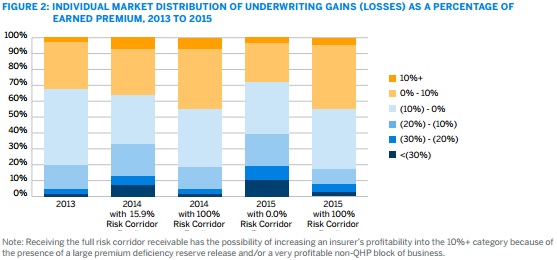

- Underwriting margins for payers selling individual plans on the health insurance exchange dropped from a 6 percent earned premium loss in 2014 to a 9.6 percent loss in 2015, Milliman recently reported. The financial losses stemmed from the Affordable Care Act’s risk corridor program funding shortfall.

Without full risk corridor funding in 2015, the proportion of individual health insurance exchange business facing underwriting losses of more than 30 percent of earned premiums increased from 7 percent in 2014 to 10 percent in 2015.

Similarly, the proportion of the exchange experiencing underwriting losses over 10 percent jumped from 33 percent to 39 percent in the same period.

Source: Milliman

HHS established risk corridor, reinsurance, and risk adjustment programs in 2014 to help private payers on the health insurance exchange adjust to Affordable Care Act changes. The 3R programs, as the three programs were dubbed, aimed to discourage payers from avoiding sicker or higher-cost individuals from enrolling in their plans. The programs provide supplemental funding to plans that include higher-risk and higher-cost beneficiaries.

In particular, the federal department developed the temporary risk corridor program to limit losses and gains that exceed an allowable range. If a payer’s spending on medical care and quality improvement activities is within 3 percent of set allowable costs, then the payer is not required to make payments to the program.

However, payers who spend below the 3 percent threshold must repay HHS a portion of the actual spending and target spending difference. In contrast, payers who spend more than the threshold will receive a payment based on how much more they spent.

The program aims to stabilize premiums by preventing payers from setting higher premiums to offset or avoid higher-cost individuals.

Milliman reported that payers qualified for $2.9 billion in risk corridor payments in 2014 and another $5.9 billion in payments in 2015.

But limited funding for the program prevented HHS from reimbursing payers the total $8.8 billion. Payers only received a total of $457 million and the payments had to go to 2014 risk corridor shortfalls first.

As a result, the report showed that almost 90 percent of the $8.3 billion program shortfall is still owed to payers who participated in the individual health insurance exchange.

The lack of full risk corridor payments to payers directly contributed to underwriting losses, the report added. If payers had received the full risk corridor payments for both 2014 and 2015, underwriting margin losses for payers selling plans to individuals on the exchange would only have been about 2 percent of earned premium.

Although, underwriting margin losses were partly offset by lower than anticipated transitional reinsurance program participation, Milliman added.

The transitional reinsurance program reimburses health plans that enroll higher-cost beneficiaries. If a beneficiary’s actual care costs exceed a set price, then the plan qualifies for a supplemental payment. The payments come from each payer contributing to the program’s funds.

In 2015, the program paid payers on the individual health insurance exchange about $1.9 billion more than expected because reinsurance contributions that year were greater than reinsurance payments in 2014.

Despite financial losses for payers, the health insurance exchange for individuals seeking coverage has gained traction among consumers since 2014. Milliman reported that health insurance exchange enrollment on the individual market grew from 15 million in 2014 to 17.5 million in 2015, even though small group enrollment declined by 2.5 million.

Researchers attributed the enrollment boost to federal premium assistance programs for consumers, such as advanced premium tax credits (APTC) and cost-shared reduction (CSR) subsidies.

Source: Milliman

Consumers may be looking more to the health insurance exchange for coverage, but the influx of enrollees may spell financial trouble for payers, especially since many receive premium assistance because of their low incomes, researchers stated.

“With this growth come changing population characteristics and corresponding pricing challenge for insurance carriers operating in the market,” Milliman wrote. “These population changes, coupled with regulatory uncertainty associated with the risk corridor program, likely contributed to the underwriting losses experienced by many individual market insurers.”

As the new presidential administration and Congress work on potential health insurance exchange reforms, Milliman intends for the financial report to inform policymakers about how the Affordable Care Act’s exchange impacts payers and consumers.

“With the United States potentially undertaking another round of health insurance reform in the near future, insurers and policymakers should study the enrollment and financial results that have occurred under the ACA [Affordable Care Act] to better understand how insurance markets may react to future regulatory and legislative changes,” concluded the report.